After that last long and rambling post catching my future readers up to date (hahah) , I’m ready to get onto a more frequent schedule. I got to thinking about the financial situation we’re in right now, which is honestly insane to me despite our spending being higher than planned, and despite the stress and related stress spending: we are way ahead of where I thought we’d be by now, but why?

First, what is our financial situation? We’re Millionaires. It’s a bit wild to write it out like that but it’s true. And with our spending under control, we are essentially financially independent. What’s crazy is just two years ago in my first financial blog post we had a net worth of $472,602. In two years we went from $472k to a cool $1M. How?

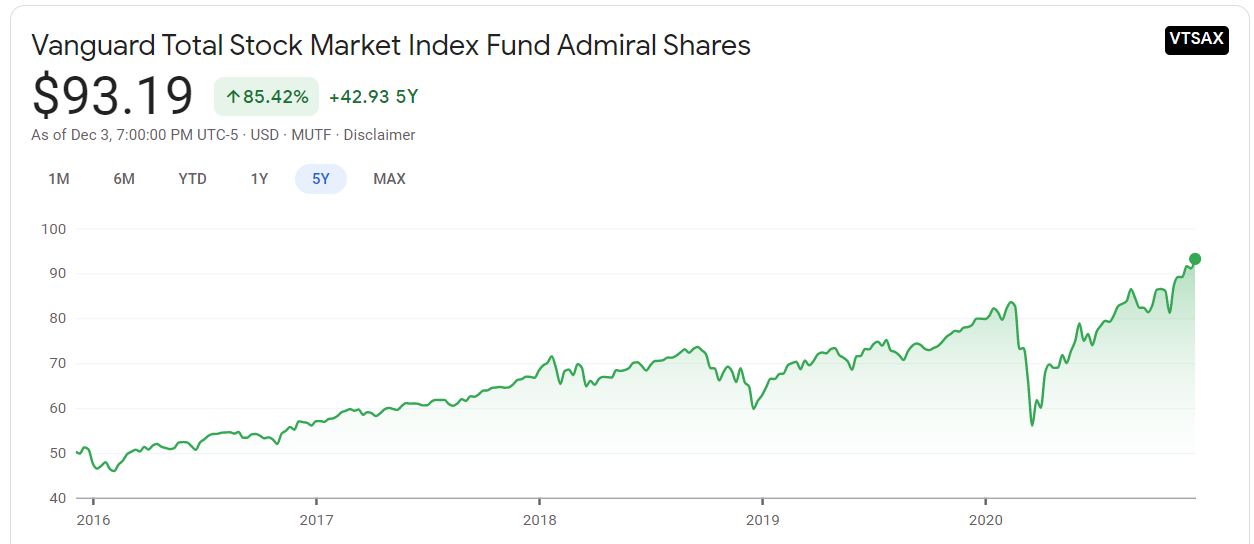

While that $472k included home equity the investment portion was ~$373k. With that let’s try an over-simplified exercise. Using VTSAX as a proxy for market performance, we can see that at 12/31/18 we were hovering around $62/share, and now we are around $93. That is a 50% increase over that time! Don’t forget dividends!

That means that before adding in the home equity then converted to shares, more bonuses, 401k’s, etc. that money we made and saved long ago fueled $187k of incremental net worth ($373 x 50%)!!

That is wild to me. In the past two years I didn’t need to actually do anything to earn that money. I didn’t even have to save more: we had already saved that money and dumped it into VTSAX. We did our part many years ago and simply left it alone.

I found this to be really powerful, and also highlights how bad we humans are at understanding the present value of money. That $50 we didn’t spend going out to dinner one night is worth a helluva lot more than $50 today. If we string many of those $5, $10, $50, and $100 decisions together it adds up really fast. Spending less is really an unstoppable wealth building machine.

I’m thankful for me and my wife from 6 years ago doing a house renovation and investing it instead of buying a luxury car, and for 22 year old me investing in my first 401k at 8% of my salary. And that’s the lesson: Current spending is more expensive than you (and I) think it is and current savings is even more powerful, because the opportunity cost or benefit is massive.

Another take on this is an article from the BBC explaining the Exponential Growth Bias. So if you’re working hard, facing challenges like how to control spending, just remember you suck at understanding exponential growth, and the benefit you are reaping is way more than it looks like!

You know, this probably applies to things besides just personal finances, which is why I’m going to shut down this computer and go lift some weights. After all I did name this blog PHYSICAL and Fiscals.