Your stuff is limiting your freedom. Don’t let it.

Every purchase should be thought of us a an anchor on a chain that wraps over your shoulders and the back of the neck that you have to carry around as long as you own the object. And when you give people gifts try and realize you are gently draping a tiny anchor on a chain over their neck albeit presented with fine wrapping paper and maybe even a bow.

Every time you purchase an item, picture everything you own, tied to a chain, wrapped around your neck and shoulders, and visualize adding yet another item.

Why? Objects take up space in your home, they use up resources of the earth, they eventually will take up space in landfills, and they represent opportunity costs that you could have invested instead. Purchasing stuff is a vote against freedom. Clutter is mentally draining, and diffuses your focus on what’s important. And the wild thing is, most of us are not conscious of how much shit we really have.

Right now, clear 10 minutes, and close your eyes. Start just mentally thinking of each room, closet, storage trunk, your attic, garage, patio or deck, or a [shudder] rented storage unit. Go deeper – within each area, think of all the objects there, squirreled away in darkness and individually consider each individual item. Hold them in your mind. The sheer volume of items is hard to comprehend. I then suggest you take a walk to each area and visually inspect it. Be in awe of the volume of your stuff. It just may make you rethink this madness.

It’s even worse if you are someone my age and still have stuff from your childhood or college at your parents’ home. You have taken many little anchors and strewn them around your parents’ necks, and it is pulling them down while the physical objects start caving in on them. It’s a bleak situation.

For certain things, the anchor is worth it of course.

Our ultra-deluxe-fancy-delicious-making-espresso machine is decidedly worth it in our house, as is our le creuset cookware. These are items that we use multiple times per week, we get actual joy when using – for example the heavy le creuset pots are by far the most enjoyable things we have to cook with, with even heat, a tight fighting lid, and colorized sides and bottom from hundreds of meals cooked in it. It’s also important to point out that these are luxuries. The vast majority of human civilization today, and also looking back over the entire timeline of the species has not been afforded such remarkable luxuries. But we’ve chosen to indulge them and they are used often and feel “real” not made of cheap plastic. But even these hallowed possessions have a deep secret we don’t often stop to think about:

They exist, even when we aren’t using them. They are part of earth’s resources that are now taking up space on my counter and cabinet. And they are only used a small amount of time of their existence. The rest of that time they just sit there, useless and in the dark, but taking up space. This is ok for items that get regular use. For the rest? What are we doing? We could be using the capital tied up in these objects to buy our freedom instead.

I’m not perfect at this either, but one of the areas of success that has helped propel us towards financial freedom, is that we don’t shop for the sake of shopping. We don’t want clutter or more things. It is the simplest thing of all: just stop buying things.

Buy second hand. Give things away to people who will actually use them. Only give meaningful gifts that people will truly benefit from (but don’t ever feel obligated to give gifts – a future article). Clear your stuff out of your parents’ home and remove the anchors around them.

Feel your life get lighter when the chains of consumption are no longer hanging from your neck.

Welp, that didn’t work out very well: After some serious plans and goals I set way back in January, 2019, along with the best intentions of blogging my journey, I’m sorry to report progress hasn’t been made.

But a lot has happened: I got a promotion with more pay, we moved to another state far away from home, and life with an almost two-year-old keeps moving forward.

But I need to make some changes. Toxic stress, lack of exercise, and being overweight is taking a toll.

We took a stay-cation last week back in coastal New England and I finally had time to take a break, play and rest on the beach, and think clearly without all of the chaos. And I recognized that I haven’t been living the life I want to live. I have been succumbing to stress and poor habits, and I’m no further to my health goals than 8 months ago.

But this is it, that’s the end of it. I want to be here for a long-time with my wife and son, set a healthy example, and just feel good!

To start this I’ve decided to make a few simple changes:

Daily exercise – even if it is 5 minutes of walking after getting ready and putting on my shoes – just start;

No processed foods, grains, or sugar (with a very broad definition of sugar);

No beer, at least for now. I may experiment with some drinks socially but I need momentum with healthy habits before messing around here;

Today was a good day. Upon waking up, I took our dog for a brisk morning walk wile my family slept soundly, I worked in the morning through early afternoon, and then we went on a family bike ride (and discovered one of my bikes was stolen! – the subject of a future post), went for a walk to play in the park, and came home for a healthy meal.

It’s a start. Today was a success: no beer, no processed foods, multiple times exercising, and family play and connection. But it’s just the beginning – see you in the next post!

It would be easy to go overboard and list every factor and measure of optimum health and personal finance here, but there’s time for that later. As I discussed in the first post you don’t want to sacrifice the perfect for the good.

Recapping the first post I noted that I weight 274.4 lbs with a BMI of 38.3, which is essentially way out of fucking control. Based on my past experience and how I feel at different weights, my long-term goal is to be a fit and muscular 200 lbs. I figure once I’m at that point I can worry about optimizing from there. Losing 74 pounds represents a weight loss of 27% of my bodyweight. Taken at this level it’s easy for a goal like this to be overwhelming, and not even to want to start. But let’s do some math:

The normal standard that any fat or weight loss institutions put forward is to aim to lose 1-2 lbs a week;

74 lbs / 2 lbs a week = 37 weeks, or roughly 8-9 months;

My reaction to this is ok great, the goal seems more achievable and also, damn I don’t want this to take 9 months.

I’m reminding myself that the process between now and my end goal is one where I’m going to feel better every single day

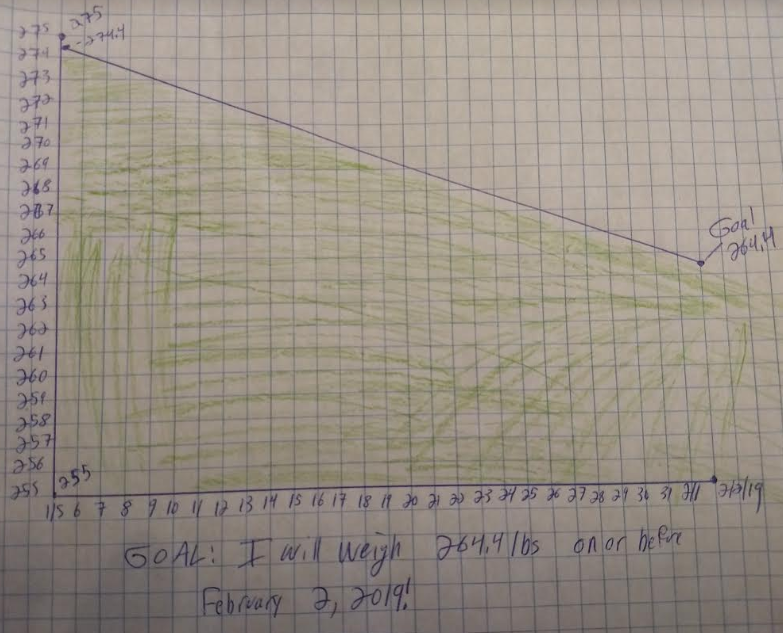

Today is January 5, 2019, therefore my goal is that on Nov 1, 2019 I will weigh 200 lbs!

To make sure I achieve this long-term goal, I’ve decided to break it down into smaller monthly goals, and then translate those to weekly/daily goals.

For the first monthly goal I’ve decided to set my check in for February 2, 2019, 4 weeks from today. I’m going to set the goal for me to be down 10 lbs by then, or roughly 2.5lbs a week, and weigh 264.4 lbs as 2/2/2019. This gives me a bit more than the 2lbs a week standard to shoot for but I believe it is still achievable, especially in the beginning.

To track my goal I’m going analog and simple. I took a piece of graph paper, and labeled the x-axis as days, and the y-axis as weight. Starting on the left I marked where I am currently, and on 2/2/2019 I marked my goal weight of 264.4. Each morning I can markdown my weight and as long as I’m below the line I drew between today and the goal date, I’m on track. If I find I’m above, it means I’m behind. Here is the graph:

I shaded in the portion of the graph below the line as green – as long as the daily tick marks are in that zone I’m on track. After I took the picture I also signed my goal statement at the bottom to ensure I felt accountable to this goal. I feel that writing out goals with affirmative statements committing to a course of action is one of the best ways to ensure you’ll achieve them.

You could of course use an app or computer program to help track this, but this is easy for me and removes any effort on a daily basis. I’ve put this in a drawer in my bathroom with a pen. It’s possible this is enough of an obstacle that I won’t look at it, but I’m hoping that isn’t the case. I could of course tape it to the wall in my bathroom, but I don’t want that information posted for whoever happens to be in our house – although I have no issue posting this on the internet apparently 🙂

So, that’s my goal and I’ll follow up in February to see how I’ve done achieving it. Of course, results don’t just materialize with no action. I need a detailed plan and I need to put it into practice.

In thinking about how to reach this goal, I’m reminded of a Charlie Munger (Warren Buffet’s friend and right hand man at Berkshire Hathaway) who said:

“The great algebraist, Jacobi, … was known for his constant repetition of one phrase: “Invert, always invert.” It is in the nature of things, as Jacobi knew, that many hard problems are best solved only when they are addressed backward.”

Inverting problems, that is, looking at them backwards or upside down, is an incredibly useful skill. Munger recommends that “Instead of looking for success, make a list of how to fail instead…” and then avoid this list of how to fail, and you will succeed. Let’s try this. If I didn’t want to lose weight, and actually wanted to add lots of pounds and become less healthy, what would I do? My list is:

Make sure I don’t get enough sleep. This will keep my cortisol levels high, and increase my hunger the next day along with lowering my willpower;

Drink soda, juice, and other sugary drinks to spike my blood sugar;

Avoid exercise at all costs so as to not burn off those precious calories and avoid lifting weights especially as if I build muscle as that will burn more calories throughout the day;

Let stress from work and other things build up and not address them, to make sure I eat and drink as a way to cope;

Eat heavily processed foods including things with MSG, artificial ingredients;

Eat sugar, which includes bread, pasta, crackers, and other things that are quickly metabolized (note: I have a pretty broad definition of sugar);

Eat beyond the point of no longer being hungry, and to help with this make sure that I’m stressed or distracted when I eat so I don’t pay attention to my body’s signals.

Avoid salads and vegetables, healthy fats, eggs, avocados, and olive oil as that will prevent me from having room for the processed foods.

Practice self-pity and negative self-talk to ensure I don’t get motivated to exercise or eat healthy;

Drink alcohol and calorie heavy drinks at that such as beer;

Holy shit, that’s a pretty scary list. But, let’s try and put in an action plan to try and avoid the pitfalls above. It’s important that I have some sort of approach or system to address habits as well. Thinking through this I’ve come up with the following:

Ensure I’m getting enough sleep. To facilitate this I’m going to do a few things:

Try to go to bed when my wife does and read my book in bed rather than staying up to help me settle down;

I’ve added a recurring phone reminder to prod me with the message “Go to bed you deserve it!” set for 9:25pm each night;

Try to limit digital devices in the evening to limit blue light that will interfere with my sleep. However, trying and hoping I do isn’t a great system so I’ve also gone ahead and download an app that reduces blue light on my phone and computer and have it set on a timer for the evening.

Don’t drink ANY sugary drinks in any portion. I’m solid on this as far as juices, soda, and other flavored drinks are. My drink of choice is seltzer water with lemon and lime.

Start a regular exercise routine, especially with weights to build muscle and burn more calories.

Just start. This is the most important thing. I have a few kettlebells and can do body weight exercises. I’ve decided that the mornings are when I’m going to commit to doing this. I have the kettlebells in my home office, and am going to clear some space so there are no obstacles at all.

Address work and other stress

Self-monitor work anxiety and emotions, and reflect on why I’m feeling that way;

Take action in the face of anxiety and stress. If I’m worried about something that may go wrong, communicate it directly to other stakeholders at work;

Take breaks during the day and go for walks and leave my desk. Don’t eat lunch at my computer.

If I can’t correct this, be open to finding a new job.

Avoid processed foods by making time, creating space, to cook ourselves (we are mostly good about this already);

I’m going to set time aside each Sunday to do some food planning, meal prep, and ingredient prep. I already enjoy cooking and use the time to listen to podcasts or audio books, and feel good about ensuring success later in the week.

Above even making our own food, ensure that I don’t eat sugar in any form including non-whole wheat bread, pasta, crackers, and similar items;

The simplest way to avoid eating these things is to not have them at the house, which means winning here is done at the grocery store. My wife currently does most of the grocery shopping so I’ve asked her to not have these things around for me;

Add in even more salads and vegetables, healthy fats and proteins like olive oils, eggs, avocados that are filling and clean burning.

I think it’s important to go into this with a sense of abundance, not scarcity. I’m not going to put in place a system where I have to track individual calories and weigh food to the gram, because I don’t think a system like that will be sustainable. What I’m going to focus instead on is eating for nutrition: eating as much salads and vegetables as my body needs, and enough healthy fats and proteins until I’m satisfied. But in no way am I restricting myself, because it won’t work for the long-run.

Say out loud to myself daily, positive affirmations, even if I don’t fully yet believe what I’m saying. This is a bit cute, silly and embarrassing and reminds of the SNL skit of Daily Affirmations with Stuart Smalley (“Doggone it people like me”), but I know I have a self-talk problem. I’m discouraged about my body and I say negative things about myself when I’m frustrated. So I’m going to over compensate for this by making a ritual out of positive self talk.

I’ve hand written this down on an index card and put it in the bathroom drawer with my weight tracker. This is how I will start my day.

My affirmation I’ve come up with is:

I [NAME], love myself;

I am in perfect health,

I am fit, healthy and loved;

I have no anxiety or worry,

My life is perfect, and I am safe and prosperous.

Limit alcohol consumption, especially beer.

I think the answer to this is to only have beer or mixed drinks socially with my friends if we are hanging out, playing games, etc;

I’m committing now to only have a beer if I “pay” for it with physical exercise. For each beer I want to consume I’ll do a set of 10 squats with the kettlebell weights, and 10 pushups or overhead presses with kettlebells.

I’m still going to leave having wine with my wife at dinner occasionally as an option;

The other items on this list are going to be key to sticking to this one. For example, getting enough sleep, exercising and addressing work stress will enable better control here.

Let’s try and sum all of that up again so it’s a more manageable list:

Go to bed when my wife goes to sleep;

Take the time to cook for myself so I always have the right foods available and have as many healthy vegetables as possible, then clean burning fats and protein. As part of food planning, don’t have bread, crackers, and other sugars in the house;

Remove obstacles to exercise and make it a daily occurance. Prioritize this time and do something even if I can’t or don’t want to do a full workout;

Face stress and anxiety with action and walk away from my desk several times a day and above all do not eat at my desk.

Daily positive affirmation each morning and night;

Enjoy beer only socially, and “pay” for each drink with lifting weights.

That’s my plan – stay tuned and I’ll provide an update on the results in February – I already know it will be a success.

I’ve dedicated this page to list the books I’ve read with few comments on my impressions of each. Have some book suggestions? List them in the comments!

January (and end of December)

Liar’s Poker by Michael Lewis

Partial autobiography of Lewis’ time in the 80’s working on Wall Street in the 1980s at Soloman Brothers;

The book is pretty wild and highlights the excesses and risk taking behaviors of Wall Street, along with the culture of greed and disappointment of big bonuses that weren’t as big as the other guys

Mortgage bond trading and the excesses of debt and risk

Definitely worth reading, Michael Lewis is a gifted storyteller

The Big Short by Michael Lewis

Later made into a movie, the book is a fascinating review of the building housing bubble in the early 2000’s and the subsequent pop.

Explains how Collateralized Debt Obligations (CDOs) turned the home mortgage into a speculative business for Wallstreet and fueled low lending standards;

Tells the story of several groups that shorted (bet it would go down) the CDO’s and the insanity of the markets at the time;

Helped me understand something I previously didn’t quite get: Falling housing prices alone have no impact on someone’s ability to pay their mortgage, so should have no impact on defaulting on a mortgage, so I never fully understood why the crash left so many defaults. The answer is that predatory lending practices resulted in teaser rates on loans for an introductory period, and then the rates would go up. The building bubble allowed under funded borrowers to simply refinance with new fees at new lower teaser rates, over and over. However, once the credit dried up and home values dropped, they couldn’t refinance, and thus defaults skyrocketed;

Interesting insights into human nature and belief, and the folly’s that can follow;

The Snowball by Alice Schroeder

Probably the most comprehensive biography of famed inventor Warren Buffet. As a longtime fan of Buffet’s approach to investing I enjoyed most of this very long book

Understanding Buffet’s path from cigar butt investing stock picker using the value investing rules handed down by Benjamin Graham, to a building Berkshire into the powerhouse it is today, in in particular the learning and changing in his approach and thinking is fascinating

Influence of Charlie Munger on Buffet’s thinking

It helps us realize that Buffet is one of a kind and no one should expect to recreate what he has done… however, there are some important lessons that if you stay rational you can do quite well.

As I alluded to in part 1, I knew we’d be a bit better of on the Fiscal side of things. Reaching Financial Independence has been a goal we’ve been working towards, and while there is definite room for improvement, we are in pretty good shape fiscally:

2018 Income and Spending:

Well, we lived on $49k for the year, and ended up with a 61.7% savings rate. Depending on who YOU are that might seem really low, or if you are more badass than us it might seem pretty high, or even extremely high. My wife’s reaction when seeing the spending numbers was discouragement that our spending was so high as we’ve been focusing on getting it lower.

Let’s also take a deeper look at where we spent those living expenses:

The good news from the above chart is that we don’t have a ton of total bullshit spending like car payments, entertainment, hired housekeepers and other home services from lawn to dog walkers, and we are usually pretty good about not shopping for the sake of it or as a fun activity or stress relief outlet. Note that “Shopping” above is anything from a story or Amazon that we haven’t categorized so could include baby stuff, definitely includes our new espresso machine (which is why coffee shop isn’t a big line item for us).

However, $38k is a shitload of money to spend for 2 people, a baby and a dog. Looking at the details we can see that Food & Dining is where we spend the lion’s share of our money at a whopping 43% of our total spend. In subsequent posts we’ll dive into these categories and see what we can do to optimize them further.

The other thing we want to understand is our total spending without mortgage interest. This is important because part of our plan to reach financial independence (have assets generating income greater than our spending, forever) includes a paid off house, so it’s useful to estimate our total spending without interest as a rough proxy for future spending. The number from 2018 is: $43,397.

A few notes re Income:

I work at my job full time, and my wife has taken the past year off to take care of our Son, who just turned 1! The income includes some trailing income from when my wife was doing paid work, but excludes a couple of things like our income tax refund;

Clearly not everyone makes this sort of income, and we’re in a good spot on this front. I’ve worked really hard to be successful in my career, but there is also privilege, luck, and the support and kindness of others involved.

If you don’t currently have an income at this level, don’t be discouraged – improvements in your finances and even Financial Independence are within your reach (read on!);

A few notes re Expenses:

I’ve split these into two categories: Living expenses and Mortgage Interest, Property Tax & Insurance.

The reason is that the Living expenses are really what we track on a monthly basis to compare how we are doing as they are what we have the easiest control over on a day-by-day basis. The housing related expenses aren’t subject to a monthly change (although of course, every expense IS a choice). This helps simplify the situation: while I can happily pour all over all of our financial details each month, this isn’t really fun for everyone, and a simple approach that

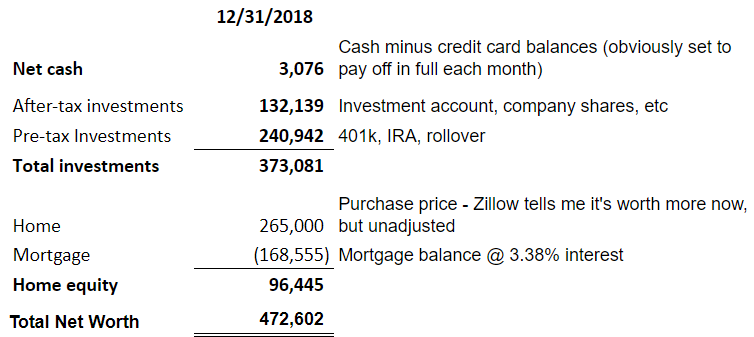

Moving on to Net Worth* as of 12/31/2018:

So we ended the year at just under half-a-million bucks of net worth. Not too shabby. This is a big pick up from when we started the year, as you can see from the fact that we had decent savings in 2018.

A few notes on Net Worth:

A traditional way of showing a balance sheet like this in a business is to show all Assets (cash, property, investments, etc), then total Liabilities (things you owe – credit cards, mortgage, student loans, etc), and then Assets minus Liabilities = Net Worth. I show it this way because it’s more useful for me for personal finance planning;

We also have two used and fully paid off cars: a Honda Fit** and a Hyundai Elantra, but we don’t include the value of those as assets, because, uh, they aren’t assets. Sorry, but cars are convenience, but we’d be fooling ourselves to think our financial position is improved by buying a car. Any money going out for personal vehicles is simply an expense;

Overall Financial Assessment

Strong income from W2 job, of which we save a respectable 61.7%;

Net Worth of $472k including $373k of investments

$43.4k of spending per year for everything excluding mortgage interest

The above equates to our investments being 8.6x our annual spending ($373k/$43.4k) – this is a key measure of our progress towards financial independence.

$169k left on the mortgage

In the next Financial post we’ll set some goals and chart the path forward including accelerating our path to 25x investments! (more on why 25x later)

Next steps for you:

Pull together a summary of your financial life. You can do this with a pen and paper, a spreadsheet, or you can get some help and automate this with a program such as Mint.com which is what I use. With Mint and similar programs, you simply link up all of your financial accounts, and it allows solid tracking of everything you need. There are some types of accounts that aren’t available to link, but you can add those manually. Then, you need to:

Start tracking your income and expenses! This is probably the most important step you can take on your journey to improved finances;

Calculate your savings rate: Remember, payments on debt count as savings. So take all of our cash outflows, less debt payments and that is your spending.

Pull together all your assets: Cash, checking/savings/money market accounts, investment accounts, 401k’s from current or former employers, IRA’s, the savings bond your grandma gave you, the loose change sitting around from when you used to be a waitress (future story coming!).

Pull together all of your liabilities, things you owe: Credit card balances, student loans, mortgage, money you owe to relatives or the IRS, other personal loans, car payments, etc.

Put together a basic Net Worth statement based on the assets and liabilities you have

At some point I’ll come back and update a spreadsheet template to make this easy;

Once you have this basic information, you know where you stand. It’s not easy to face our own problems square in the eye, but it’s the only way to start improving.

See you on the next post!

*A note on “Net Worth” – this is normal terminology for equity, and really the formula of Assets minus liabilities. However, the Mrs. really dislikes this term, because clearly a person’s “worth” is far more than their financial standing. No argument here, however, for simplicity we’re sticking with the perhaps outdated term “Net Worth.” **Another note from the Mrs re the Honda Fit: “The freaking best car ever with 6 airbags, 8 cup holders, and plenty of room for 2 adults, a happy dog, and a rear facing car seat in the middle position.”

First thing’s first – where are we at today both physically and fiscally? Well, in my case I know I’ve got a gap on the physical aspects, and fiscally we’re in much better shape, but with room to improve. That’s why today I’m going to focus on the physical.

It’s tempting to create a detailed spreadsheet (ok, it’s only tempting for the Finance guy) with all of the different attributes of health and fitness, and track each of those going forward with goals for each. But just thinking about that is overwhelming, and then trying to action each piece is even harder, and sometimes you just don’t want the perfect idea to get in the way of the good. There will be time for nuance and optimization, but right now I have an emergency for the physical side:

Weight: 274.4 lbs

Height: 5’ 11” (71 inches)

BMI: 38.3, Obese (woof, but also note, you can use this handy BMI calculator)

Body Mass Index (BMI) Categories:

Normal weight = 18.5–24.9

Overweight = 25–29.9

Obesity = BMI of 30 or greater

They also have a handy BMI chart, so we can look up and see at what weight is for your height at each category. For someone 71 inches tall like myself, it shows that 208-215 pounds (corresponds to a BMI of 29/30, respectively) is the range when I’m no longer considered obese, just overweight. Now, there are many limitations with BMI and it doesn’t take into account body composition (fat vs muscle), but that isn’t really the point. The point is I have a huge fucking problem here. Carrying this much weight isn’t comfortable physically or emotionally or healthy, and I have a son now and I want to set a good example.

Adding a bit more complexity, my weight is a symptom of a few key things within my control:

My reaction to stress from work, life etc,

Lack of physical exercise

Alcohol consumption as a way of dealing with stress

I will be totally truthful – this wasn’t easy to write out or think about. However, I have a few options right now:

Ignore the problem and pretend it isn’t there;

Complain and blame the societal forces, work stress, the political climate, tin-foil hat theories, and the like as an explanation for my weight;

Take action into my own hands and change my situation today!

The third option is the only logical one, and a big part of why I’ve started this blog. Stay tuned, things are going to change.